what is safe note india? The India Founder Guide to the Agreement That Seems Simple and Rarely Is

Definition

A SAFE note (Simple Agreement for Future Equity) is an investment instrument where an investor gives a startup money today in exchange for the right to receive equity at a future funding round — at a discounted price or capped valuation. For Indian founders, it is one of the fastest ways to close an early cheque without negotiating a valuation upfront. Unlike the US, where SAFEs are standardised by Y Combinator, Indian SAFE notes vary significantly investor to investor — making the specific terms far more important than the name on the document.

Pre-Seed

Also Angel rounds

₹25L–2Cr

Typical angel cheque

Valid

Under Companies Act 2013

1–3 wks

vs 4–8 wks for equity

Why Every Indian Founder Needs to Understand This Before They Sign

Imagine you are a founder in Bengaluru. You have built something real — 200 paying customers, ₹8 lakh in monthly recurring revenue, and a product that works. An angel investor you respect offers ₹50 lakhs. She does not want to negotiate a valuation today — she suggests a SAFE note. You look it up online. Everything you find is from Y Combinator, written for American founders, referencing American law and American deal norms. You sign because you trust her and you need the capital.

Three years later, at your Series A, the cap table conversation gets complicated. The conversion mechanics of that early SAFE — the discount rate, the valuation cap, the MFN clause — all of it comes back to the table at the exact moment when you have the most to lose and the least leverage.

This post exists so that scenario does not happen to you. Not because SAFE notes are bad instruments — they are not. But because the founder who signs one without fully understanding the mechanics is playing a game where the other person knows the rules and they do not.

Why SAFE Notes Work Differently for Indian Founders

In the United States, a SAFE note is a near-standard instrument. Y Combinator publishes its template publicly and most US angels are comfortable with the YC format. In India, no such standard exists. An Indian SAFE note is a bespoke document — every investor drafts or modifies their own version. That means two SAFE notes signed in the same month from two different angels in the same city can have materially different economic consequences for the founder.

From a legal standpoint, SAFE notes are valid in India under the Companies Act 2013 — but they sit in a grey zone that is worth understanding. Because a SAFE note is not technically debt (no interest, no repayment obligation) and not yet equity (no shares are issued at signing), it occupies a contractual middle ground. For Indian startups with foreign investors or NRIs, FEMA (Foreign Exchange Management Act) regulations become relevant — specifically, pricing guidelines under the Foreign Exchange Management (Non-Debt Instruments) Rules, 2019 apply at the point of conversion. A founder who does not account for this at the SAFE stage may face complications at the equity conversion stage. Consult a startup-focused CA or lawyer when foreign capital is involved.

How a SAFE Note Works in India — Explained Clearly

A SAFE note has one core mechanism: money comes in today, equity gets issued later. The “later” is triggered by a defined event — usually a priced equity round (your Seed or Series A). Here is what the mechanics look like in practice.

The investor writes a cheque today — with no valuation negotiation

An angel agrees to invest ₹50 lakhs. Instead of negotiating what percentage of your company that ₹50L is worth right now — which requires agreeing on a valuation — both sides agree to figure that out later. The investor signs a SAFE note, you receive the capital, and no shares change hands yet.

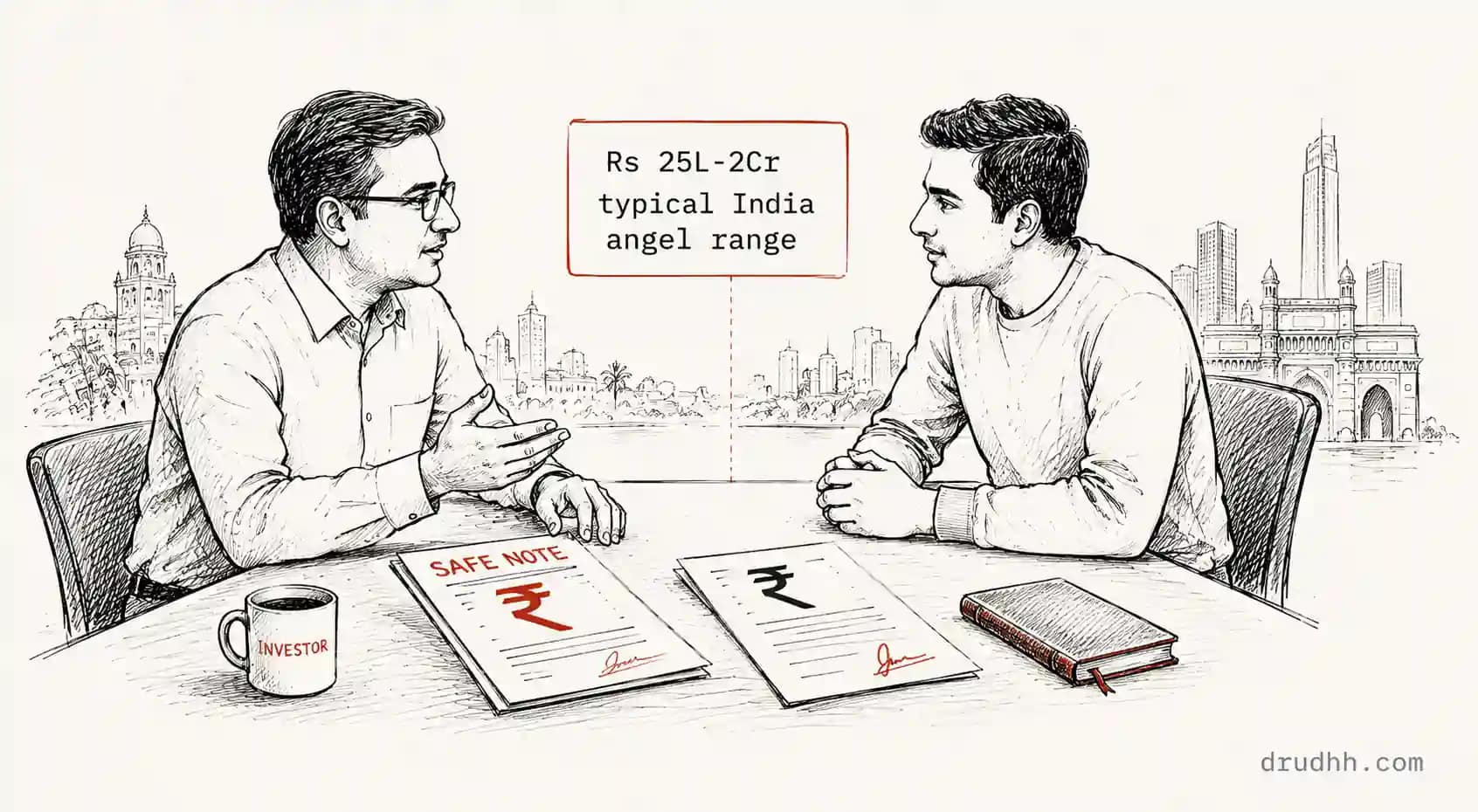

India note: Indian angels typically issue SAFE notes between ₹25 lakhs and ₹2 crore. Above ₹2Cr, many angels prefer a priced round or convertible note instead.

Common mistake: Founders assume “no valuation negotiation today” means “no valuation risk ever.” It doesn’t — it defers that risk to the next round, when it becomes a harder conversation.

The valuation cap and discount rate are the two most important terms

A valuation cap sets the maximum company valuation at which the SAFE investor converts — protecting them if the company grows significantly. A discount rate gives them a percentage off the price per share at the next round (typically 15–25% in India). Most SAFEs have one or both. If your next round values you at ₹20 crore and the SAFE cap was ₹10 crore, the investor converts as if your valuation is ₹10 crore — meaning they get more shares for the same money.

India note: Valuation caps of ₹5–15 crore are common for pre-seed SAFEs in India. Angel networks like LetsVenture or Indian Angel Network deals tend to run slightly higher.

Common mistake: Founders sign a SAFE with an aggressive valuation cap without modelling how it will dilute them at Series A if the company performs well.

The trigger event converts the SAFE into equity

When your company raises a priced equity round — typically a Seed or Series A — the SAFE automatically converts into shares. The conversion price is calculated based on whichever is more favourable for the investor: the valuation cap price or the discount price. This conversion happens without additional negotiation. The investor does not need to “re-agree” to anything — it is contractually automatic once the trigger event occurs.

India note: Conversion at a Seed round is most common. Some Indian SAFEs also include a dissolution clause — if the company shuts down before a priced round, the investor gets their capital back before founders. Understand this clause before signing.

Common mistake: Not building a cap table model that shows post-conversion dilution. You need to see the number before Series A — not during it.

The MFN clause — the one most founders underestimate

MFN stands for Most Favoured Nation. It means: if you give any future SAFE investor better terms than this investor got, this investor automatically gets those better terms too. This clause exists to protect early angels — but for founders, it means every SAFE you sign after the first one is connected to the first. If you give your third angel a lower cap, angels one and two get that lower cap automatically.

India note: MFN is increasingly common in Indian angel SAFE notes — especially from more sophisticated angels who have seen how it plays out. Assume it is there until you verify it is not.

Common mistake: Stacking multiple SAFEs without tracking MFN exposure across all of them. Maintain a master SAFE register from day one.

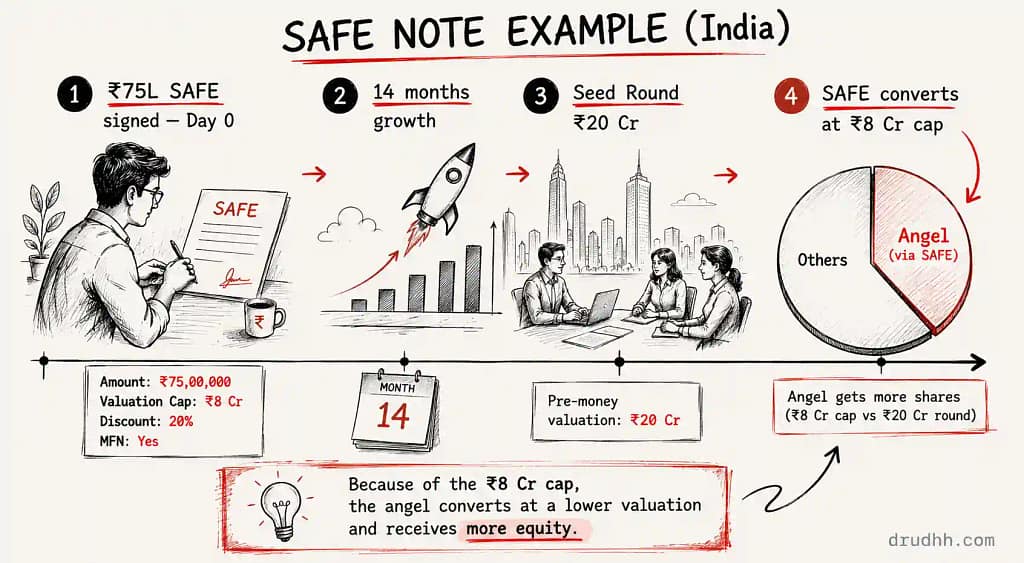

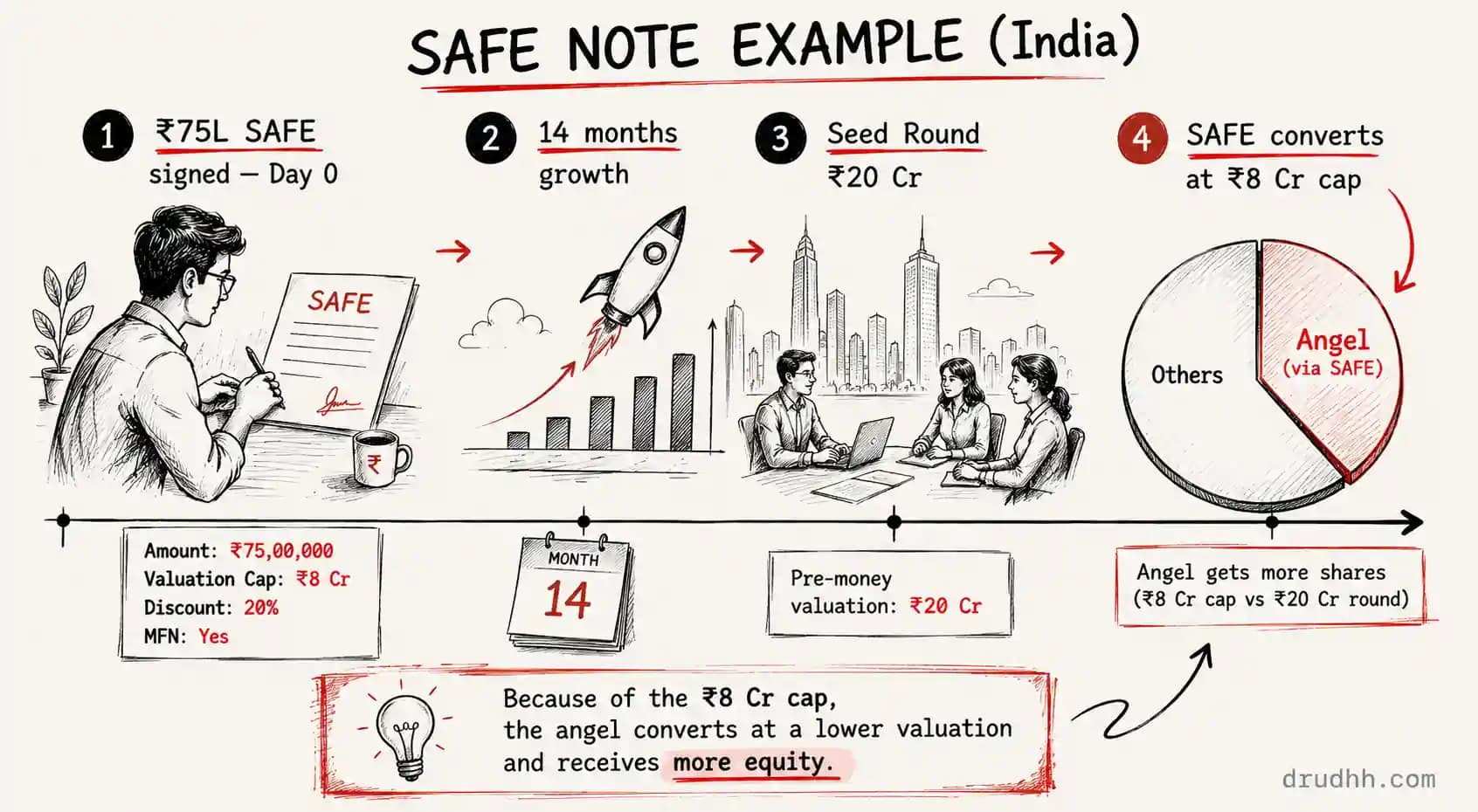

A Real Example — India Context

Example — Pre-Seed SAFE, IndiaImagine Arjun, who has built a B2B logistics SaaS product in Pune. His company is 8 months old — ₹6 lakh MRR, no institutional funding yet. A seasoned angel investor from Mumbai, who has backed 12 startups through LetsVenture, offers ₹75 lakhs on a SAFE note.

The terms: ₹8 crore valuation cap, 20% discount, MFN clause included.

Arjun takes the capital and grows. Fourteen months later, he raises a Seed round at a ₹20 crore pre-money valuation. At conversion, the angel’s ₹75L converts using the cap price (₹8Cr), not the round price (₹20Cr) — because the cap gives a better deal. The price per share at the cap is ₹8Cr ÷ total shares, which means the angel gets significantly more shares than if she had simply bought in at the Seed price.

Arjun is diluted more than he expected — but because he ran the cap table model before signing, he was prepared for it. He had built the dilution into his Seed round target size. The founder who does not model this in advance is the one who gets surprised in the boardroom.

What Indian Founders Get Wrong About SAFE Notes

Mistake 1: Signing without a valuation cap — or with a cap that is too low

A SAFE with no valuation cap means the investor converts at the next round price with only the discount. That sounds fine — until your company 10x’s and the angel converts at a price that is still deeply favourable, diluting you far more than you expected. Equally, a cap set too low relative to your actual traction locks in aggressive dilution before you even reach Seed. This can make your cap table unattractive to institutional investors at Series A.

Fix: Model dilution at 3x, 5x, and 10x growth scenarios before agreeing to any cap number.

Mistake 2: Not understanding MFN clause exposure across multiple SAFEs

Most founders sign their first SAFE carefully. Then they sign a second, a third. Each one potentially has MFN provisions. If your third SAFE has a lower cap than your first, that lower cap applies retroactively to your first angel — who now gets more shares than you agreed to give them. Most Indian founders discover this at the worst possible time: during Series A due diligence.

Fix: Build a SAFE register from day one. Every SAFE you sign — date, amount, cap, discount, MFN status. Review it before signing each new one.

Mistake 3: Using a US-format SAFE without India-law review

The Y Combinator SAFE template is excellent — and almost entirely written for US law. Governance rights, conversion mechanics, and dissolution clauses reference US-specific frameworks that do not map cleanly to the Companies Act 2013. Founders who use a YC SAFE template without modification for an Indian investor relationship can end up with a document that is valid but creates ambiguity when it matters most — at conversion.

Fix: Always have any SAFE reviewed by a startup-focused Indian lawyer before signing — especially if there is a foreign investor involved (FEMA compliance is mandatory).

Mistake 4: Stacking too many SAFEs before a priced round

Raising ₹50L on a SAFE, then ₹30L on another, then ₹40L on a third feels like clean, fast capital. But by the time you reach your Seed round, you have three SAFEs converting simultaneously — each at different caps and discounts. The cumulative dilution can surprise both you and your new institutional investors, who may push back on your pre-money valuation or your post-conversion cap table. Three SAFEs converting at once can mean 15–25% dilution before the Seed investor even gets in.

Fix: Set a total SAFE raise limit before you start (in rupees). Close it, model the full conversion, then go to a priced round.

Mistake 5: Treating a SAFE as a “safe” way to avoid the hard conversation

SAFE notes do not eliminate the valuation conversation. They defer it. The founder who signs a SAFE because they do not want to negotiate valuation today will negotiate valuation later — at Series A, with more investors in the room, higher stakes, and less leverage. The deferred question always returns. The only question is whether you are prepared for it when it does.

Fix: Know your target valuation range before you sign any SAFE. The cap you agree to should be consistent with where you expect to raise your priced round.

My Take — SAFE Notes in India

“A SAFE note is not a founder-friendly instrument. It is a founder-convenient instrument — and that is a very different thing.”

Convenience is real. A SAFE closes faster, requires less negotiation, and lets you take capital from an angel without spending six weeks on a shareholder agreement. For a founder who needs ₹50 lakhs in the next 30 days to hit a product milestone, that speed has genuine value.

But convenience is not the same as protection. The investor’s lawyer did not draft the SAFE to protect you. The valuation cap, the MFN clause, the conversion mechanics — these are all instruments that protect the investor’s capital. That is not malicious. That is the function of the document.

The founders who use SAFEs well understand exactly what they are deferring and at what cost. They run the dilution model. They cap their total SAFE exposure. They keep a register. The ones who get hurt at Series A are the ones who signed quickly because the document looked simple and the investor seemed trustworthy. Both of those things can be true — and the conversion math can still surprise you two years later.

Drudhh’s recommendation: Use a SAFE when speed genuinely matters and you have done the dilution math. Do not use it as a shortcut around a conversation you should be having.

Frequently Asked

what is safe note india ?

A SAFE note (Simple Agreement for Future Equity) in India is an investment contract where an investor provides capital to a startup today in exchange for the right to receive equity at a future priced funding round. It is used primarily at the pre-seed and angel stage to avoid the time and complexity of negotiating a full valuation. Unlike its US counterpart, the Indian SAFE note has no standardised format — every investor may use a different version with different terms.

How does a SAFE note work for Indian startups?

An investor writes a cheque to the startup — typically between ₹25 lakhs and ₹2 crore in the Indian angel context — and receives a SAFE note in return. No shares are issued at this point. When the startup raises a priced equity round (usually a Seed or Series A), the SAFE automatically converts into shares. The conversion price is determined by the terms in the SAFE — either a valuation cap (a maximum price) or a discount rate (a percentage off the round price), or both.

Is a SAFE note legal in India?

Yes, SAFE notes are legally valid in India and are used in angel and pre-seed rounds. They are governed by contract law and, at conversion, by the Companies Act 2013. Founders raising SAFE capital from foreign investors or NRIs must ensure FEMA compliance — specifically, the Foreign Exchange Management (Non-Debt Instruments) Rules, 2019 apply at the point of equity conversion. Consult a CA or startup-focused lawyer for advice specific to your situation.

How is a SAFE note different in India vs the US?

In the US, Y Combinator’s SAFE template is widely adopted as a near-standard document — most angels and founders use the same base format. In India, no such standard exists. Every Indian SAFE is a bespoke document drafted by the investor or their lawyer. This means terms, clauses, and protections vary widely. Indian founders should not assume any two SAFEs are equivalent — always read and compare the actual terms, not just the name of the instrument.

When should an Indian founder use a SAFE note?

A SAFE note makes sense when you need capital quickly, cannot establish a defensible valuation yet, and your investor is comfortable with the instrument. It works best for pre-seed and early angel rounds in India — typically ₹25 lakhs to ₹1.5 crore. It is less suitable when the investor is an HNI who prefers debt-like structures, when you already have significant traction that supports a priced round, or when you have already signed multiple SAFEs and additional conversion would create cap table complexity at your next raise.

What are the risks of a SAFE note for Indian founders?

The primary risks are unexpected dilution at conversion, MFN clause exposure across multiple SAFEs, and cap table complexity at the Series A stage. A founder who stacks three or four SAFEs with different caps and discount rates may find that the cumulative conversion — when it finally happens — dilutes them 20–30% before institutional investors even enter. Additionally, SAFEs with dissolution clauses mean investors recover capital before founders if the company shuts down before a priced round.

What is the difference between a SAFE note and a convertible note in India?

A SAFE note is not debt — there is no interest rate and no repayment date. A convertible note is a loan that accrues interest and has a maturity date by which it must either convert to equity or be repaid. In India, convertible notes are more familiar to traditional investors and HNIs who prefer debt-like instruments. SAFEs are cleaner and faster to close, but convertible notes offer investors more protection if the company does not reach a priced round. The right choice depends on investor preference and deal context, not on which sounds better.

Are SAFE notes commonly used in Indian startup funding in 2026?

Yes — SAFE notes have grown significantly in adoption in Indian early-stage funding through 2025 and into 2026, particularly in angel and pre-seed rounds facilitated by platforms like LetsVenture, Ah! Ventures, and Indian Angel Network syndicates. They remain less standardised than in the US, and usage is concentrated at the pre-seed stage. Institutional VCs in India — including funds like Blume Ventures, Accel India, and Peak XV — typically prefer priced rounds from Seed onwards and will want to see a clean cap table with SAFEs already resolved or structured clearly before they invest.

Also on Drudhh

Rapido Isn’t Just Fighting Uber.

It’s Building India’s Next Mobility Layer.

A deep dive into Rapido’s business model,

unit economics, investor confidence,

competitive positioning and what the

company’s trajectory says about India’s

mobility market.

Disclaimer: This post is for educational purposes only and is not legal, financial, or investment advice. SAFE note structures, FEMA applicability, and regulatory requirements can vary significantly based on your specific circumstances. For advice specific to your startup’s situation — including any foreign investment, FEMA compliance, or cap table structuring — consult a qualified CA or startup-focused lawyer in India.

About Drudhh: Drudhh.com covers India startup funding, VC activity, and founder education — independently, every week. We track angel rounds, institutional deals, and the trends that matter to Indian founders building in 2026. Published every Monday, Wednesday, and Friday.