Urban Mobility

Unicorn

Founded 2015

Bengaluru

Rapido Deep Analysis : The Startup Rewiring Urban Transport in India

A full breakdown by Drudhh Editorial Team — May 20, 2026

The Short Version

In May 2026, Rapido raised $240 million led by Prosus — part of a $730 million combined primary and secondary deal that values the company at $3 billion. That number would have been unimaginable in 2015, when three engineers in Bengaluru spent months pitching a bike taxi idea to 75 investors who all said no. Rapido today operates in more than 400 Indian cities, supports over 9 million driver-partners (called captains), and reported ₹934 crore in operating revenue for FY25 — a 44% jump in one year. With Uber’s own CEO calling Rapido India’s toughest competitor, and an IPO on the horizon, this is the moment to understand what Rapido actually is, how it makes money, and whether the $3 billion valuation is justified.

Who Built This — and Why

Three Engineers, 75 Rejections, and One Observation About Traffic

Pavan Guntupalli was sitting in Bengaluru traffic in 2014 when the obvious became undeniable. Cars and autos were going nowhere. Bikes were slipping through gaps that didn’t exist for anything with four wheels. He had already failed at six startups. He had co-founded theKarrier with Aravind Sanka — a mini-truck logistics platform that briefly worked, then didn’t. The pair had burned through ideas and investor rejections at a pace that would have stopped most people.

What Pavan saw in that traffic jam was not a product problem. It was a category problem. Every ride-hailing platform — Ola, Uber, Meru — had built for cars. Nobody had built for the vehicle that India’s roads actually favoured. Two-wheelers were faster in city traffic, dramatically cheaper to operate, and already the transport of choice for hundreds of millions of Indians who had never once considered calling a cab. The insight was simple. The execution was not.

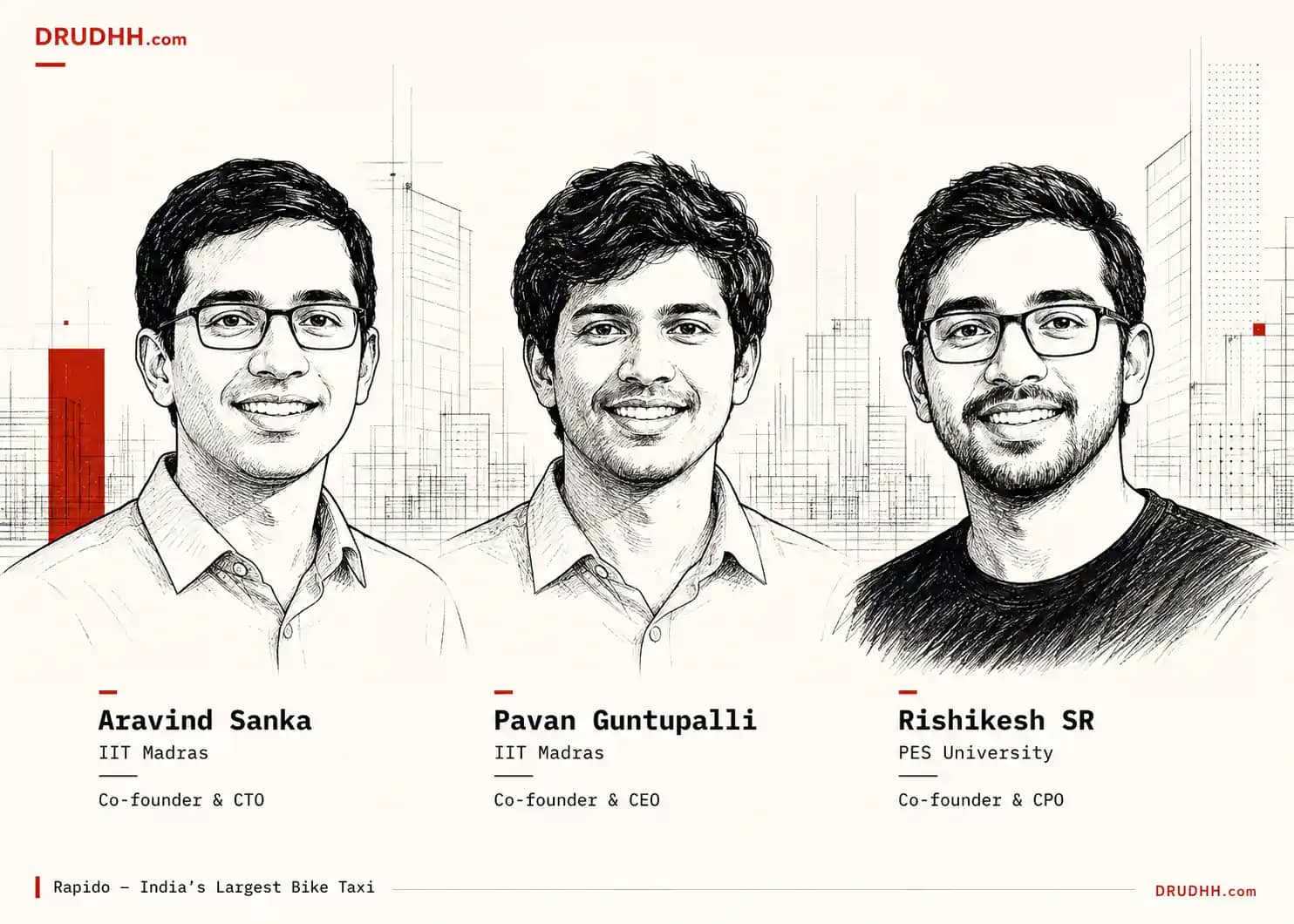

Sanka brought Flipkart’s supply-chain thinking; Guntupalli brought Samsung’s software discipline; Rishikesh SR brought the raw hunger of a serial founder who had already failed and refused to quit. The three launched Rapido in 2015 in Bengaluru with a base fare of ₹15 and a per-kilometre rate of ₹3 — roughly half the cost of any cab alternative. Within months, they were clocking 30,000 rides per day. Within a year, Hero MotoCorp’s Pawan Munjal and former Google India head Rajan Anandan had both backed them.

The seventy-five rejections that preceded Munjal’s yes are worth noting — not for the drama, but for what they reveal about timing. The investors who said no were not wrong about the risks; bike taxis were legally prohibited in several states. What they missed was the size of the market that existed in the gap between what was legal and what people actually needed. Rapido built into that gap and eventually changed the regulatory conversation in most states where it operated.

The Money Trail

From ₹15 Lakh Seed to a $3 Billion Valuation in Eleven Years

Angel Round

May 2015

Smile Group

2016-19

WestBridge · Nexus

Apr 2019

Shell Ventures

Aug 2021

Swiggy · TVS

Apr 2022

WestBridge · Prosus

Jul 2024

Prosus · WestBridge · Accel

May 2026

Announced Intent

| Date | Stage | Amount | Lead Investor(s) | Valuation |

|---|---|---|---|---|

| May 2015 | Seed | $181K | Sol Primero, Outbox Ventures, Angels | N/A |

| 2016–2019 | Series A | ~$5M | Smile Group, Nexus (Tranche 3), Pawan Munjal | N/A |

| Apr 2019 | Series B | ~$25M | WestBridge Capital, Nexus Venture Partners | ~$100M |

| Aug 2021 | Series C | ~$52M | Shell Ventures | ~$350M |

| Apr 2022 | Series D | $180M | Swiggy, TVS Motor Company, WestBridge | $830M |

| Jul 2024 | Series E | $200M | WestBridge Capital, Prosus (Dec 2024 ext.) | $2.3B |

| May 2026 | Series F | $240M | Prosus, WestBridge Capital, Accel | $3.0B |

Three facts about this cap table are worth pausing on. First, the Swiggy exit. Swiggy led the Series D in 2022, taking roughly a 12% stake. In September 2025, it sold the entire position to Prosus and WestBridge for approximately ₹2,400 crore — a 2.5x return in three years. That exit validated Rapido’s trajectory while simultaneously concentrating ownership in hands that are aligned with a longer horizon.

Second, Prosus’s conviction. The Dutch technology investment group first invested in December 2024, then anchored the May 2026 Series F. Prosus does not make incremental bets. Its India mobility conviction now sits alongside its positions in Meesho, PayU, and others — a signal that Rapido’s addressable market is seen as genuinely large.

Third, the secondary layer. Beyond the primary raises, a September 2025 secondary transaction of approximately $271 million involved existing shares changing hands — TVS Motor and Swiggy exiting, Prosus and WestBridge deepening. This is not new capital into Rapido’s treasury, but it matters: it sets a price, creates liquidity for early shareholders, and tightens the relationship between Rapido and its highest-conviction backers heading into a likely IPO.

How This Business Actually Works

Not a Tech Company. Not Exactly a Transport Company Either.

Pays fare upfront

Commission + Subscriptions

Fare minus commission

Parcel + Ownly food

~10–15% of GOV est.

What it sells and to whom. Rapido connects passengers — mostly daily commuters making short urban trips — with bike taxi captains for a ride. The core customer is someone who is too far to walk, too time-pressed to wait for a bus, and for whom a ₹50–80 cab feels like an indulgence. Rapido’s bike rides typically cost ₹20–60 for a 3–8 km journey. The platform is B2C at scale, with a two-sided marketplace that needs both riders and captains dense in the same geography to work.

How it makes money. Rapido’s primary revenue stream is commissions on completed rides across bike, auto, and cab categories. Captains pay either a daily subscription fee (a fixed amount regardless of rides) or a per-ride commission, depending on the market and vehicle category. This subscription model is intentional — it gives Rapido predictable revenue and incentivises captains to do more rides to justify their fixed cost. Secondary revenue comes from Rapido’s delivery arm (parcel and logistics), the Ownly food delivery platform, and incipient financial services through its Shyogsamart subsidiary.

Unit economics — what the numbers suggest. Rapido’s FY25 Gross Order Value (GOV) is not separately disclosed for that year, but FY24 GOV was ₹4,257 crore on ₹648 crore operating revenue — implying a platform take rate of approximately 15.2% of GOV. At FY25’s ₹934 crore revenue and applying a similar take rate, Drudhh estimates FY25 GOV at approximately ₹6,100–6,500 crore. The company spent ₹1.35 to earn ₹1 of operating revenue in FY25, down from a worse ratio in prior years — indicating improving but still pre-profitability unit economics.

The path to profitability. Rapido’s EBITDA margin was negative 19.59% in FY25, improving from approximately negative 40%+ in FY23. The levers are clear: fixed cost reduction per unit (already demonstrated — 50% reduction on a per-unit basis in Q2FY25), higher GOV with existing infrastructure (density helps margins at scale), and category expansion into higher-margin businesses like financial services. The company does not need to reinvent its economics — it needs GOV to grow faster than costs, which it is doing.

The Numbers — What We Know and What We Estimate

Revenue Growing Fast. Losses Narrowing Faster.

₹934 Cr

Operating Revenue · FY25

+44% YoY · Source: RoC filings

(₹258 Cr)

Net Loss · FY25

Narrowed 30.5% from ₹371 Cr in FY24

₹4,257 Cr

Gross Order Value · FY24

~2x growth YoY · FY25 GOV not disclosed

−19.6%

EBITDA Margin · FY25

Improving from ~−40% in FY23 · Source: Entrackr

$3.0B

Valuation · May 2026

Post-money · Series F · Business Standard

9M+

Driver-Partners (Captains)

400+ cities · Source: Company, May 2026

The revenue trajectory tells the clearest story: ₹443 crore in FY23 → ₹648 crore in FY24 → ₹934 crore in FY25. That is a compounding growth rate of approximately 45% per year. More importantly, losses are narrowing faster than revenue is growing — from ₹675 crore in FY22 to ₹371 crore in FY24 to ₹258 crore in FY25. The arithmetic points toward operational breakeven in FY27 if the trajectory holds, though the new $240 million in capital will likely fund accelerated expansion that temporarily widens losses again before narrowing them at a higher scale.

Who Else Is Playing This Game

Uber Called Them Their Toughest Indian Rival. That Line Deserves Unpacking.

X-AXIS: GEOGRAPHY

Tier-2/3 Cities →

● Competitors

| Company | Founded | Total Funding | Revenue (Latest) | Status |

|---|---|---|---|---|

| Rapido | 2015 | $800M+ | ₹934 Cr (FY25) | Unicorn · $3B |

| Uber India | 2013 | Global listed | N/A (consolidated) | NYSE Listed |

| Ola Cabs | 2010 | ~$3.8B | ₹2,800 Cr (FY23) | Private · Losses |

| Namma Yatri | 2022 | $4.4M | Early stage | Seed Stage |

| BluSmart (EV) | 2019 | ~$170M | Ops Suspended ’25 | Troubled |

Uber CEO Dara Khosrowshahi called Rapido his toughest competitor in India — ahead of the better-known Ola. That framing is precise for a reason. Rapido does not compete with Uber on premium four-wheeler rides in South Mumbai or South Delhi. It competes with Uber on the bike taxi layer, on auto-rickshaws, and increasingly in the Tier-2 cities where Uber has yet to build density. Ola, meanwhile, has been distracted by its electric two-wheeler business and a series of execution missteps in its core mobility platform.

Drudhh’s honest take on competitive position: Rapido’s moat is not technology — any platform can replicate an app. The moat is supply-side density: 9 million captains who are economically dependent on Rapido’s platform, trained in its systems, and would face significant switching costs to move to a competitor. That supply density is genuinely hard to replicate quickly. The risk is that Uber, with its global balance sheet, could subsidise a supply-side buildout in Indian Tier-2 cities. Rapido must win those markets before Uber gets there — which is precisely what the $240 million is for.

The Size of the Prize

India Has 400+ Cities. Rapido Seriously Works in Maybe 50 of Them.

India’s urban mobility market is not a monolith. The organised ride-hailing slice — the part that platforms actually capture — sits inside a much larger informal market of autos, buses, shared jeeps, and bicycles. Drudhh’s approach to the TAM: India has roughly 500 million urban residents. If 30% make at least one paid urban trip per day at an average fare of ₹60, that is a ₹3.3 lakh crore annual market — of which organised ride-hailing currently captures perhaps 5–7%.

Within that, the bike taxi segment is structurally underserved. Two-wheelers account for roughly 75% of registered vehicles in India, and the average trip distance in Indian cities is under 6 km — perfect for a bike ride. The India ride-hailing market is expected to grow at a CAGR of approximately 14–16% through 2030, driven by smartphone penetration in smaller cities, rising urban migration, and the formalisation of gig work.

The specific bet Rapido is making is that Tier-2 and Tier-3 cities — which account for roughly 65% of India’s urban population but less than 30% of current organised ride-hailing GMV — are the next decade’s growth engine. Rising incomes, smartphone adoption, and the absence of established competitors in those markets create a window that will not stay open indefinitely.

What Could Go Wrong

The Risks That Rapido’s Funding Round Didn’t Solve

High

High

Medium

Medium

Medium

Low

The Road Ahead

Three Possible Futures for a Company at $3 Billion and Climbing

Rapido co-founder Aravind Sanka confirmed an IPO intent by end of 2026. The $240 million Series F is being deployed to expand in Tier-2 and Tier-3 markets, grow the captain network, scale Ownly in more cities, and invest in platform technology. The next 18 months will determine which of three futures unfolds.

DRUDHH’S VERDICT — Rapido

The Case For

The Case Against

Frequently Asked

Everything You Need to Know About Rapido

Latest India Startup Funding This Week →

This Week’s Funding Analysis →

More Startup Deep Analyses →

About This Analysis

Published: May 21, 2026. Last updated: May 22, 2026. This analysis was prepared by the Drudhh Editorial Team using information from public RoC filings, Business Standard, Entrackr, MediaNama, Tracxn, and official company announcements. Financial figures are sourced from Registrar of Companies filings unless labelled “Estimated” or “Reported.” Estimates are clearly labelled with methodology. Drudhh operates independently and has no advertiser relationships with any company covered. This is editorial analysis, not investment advice. To flag corrections or errors, comment below